White Natural Versatile Plastic

Option Wedge

Made by

Print With Shapeways

Choose Your Material

Choose Your Material

Choose your color and finish

Choose your color and finish

$42.49

Have a question about this product?

contact the designerYou must be logged in and verified to contact the designer.

Product Description

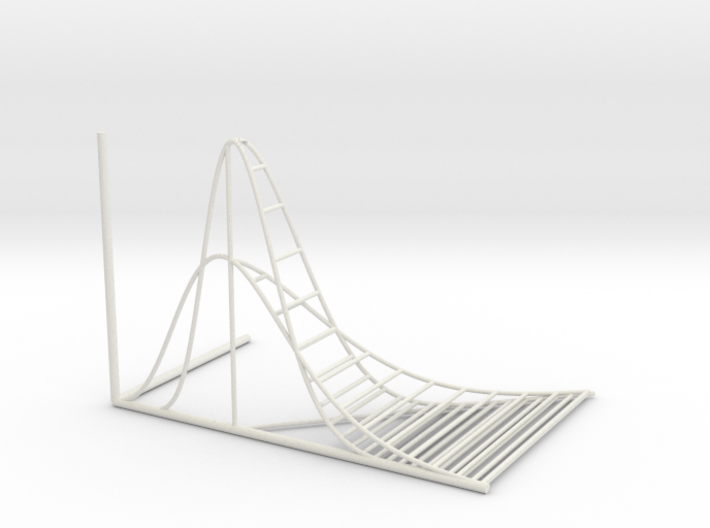

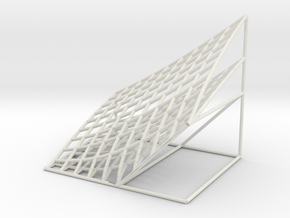

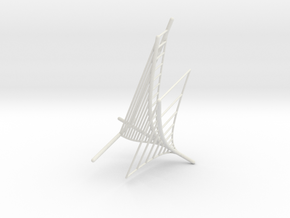

The volume defined by the payout of a call option (on the y axis, depth) and the lognormal distribution (z axis, height) of the price of the underlying stock (on the x axis, width). Roughly equivalent to what the Black-Scholes-Merton formula calculates and discounts to the present. Two stocks are displayed, one with small standard deviation (thin tails) and one with large (fat tails). I am offering this with no markup.

Details

What's in the box:

OptionWedge20171026

Dimensions:

Success Rate:

First To try.

What's this?

Rating:

Mature audiences only.

{kind=link}